2026 Outlook: Part 2

My top ideas for 2026

Happy new Year!

As we turn the page to 2026, I want to thank you for reading and following my research. This substack exists because of your engagement and support, and knowing that analysis like this provides value to you is my biggest motivation to keep writing.

This was the first year I started doing real fundamental work, beyond just reading Twitter threads about why XXX company is worth owning. I began to look into sell side research reports, listened to earnings calls, went through filings, searched for analyst communities and Substack writers I admire, and tried every way I could to learn from industry experts.

The more I learned throughout this process, the more I realized how much I don’t know, and that’s probably the most important lesson I’m carrying into next year.

Let’s jump in for part 2 and see what are my top ideas.

My Decision Framework

In Part 1 of my 2026 outlook, I laid out the general market setup, including the AI bubble debate and why valuation is the main overhang heading into 2026.

When the starting valuation is elevated, I’m relying more earnings growth rather than multiple expansion. So my ideas for 2026 narrows to two buckets.

Companies where operational execution and earnings power can keep extending gains.

If the business compounds faster than expectations, strong earnings growth is the best way to compress valuation overtime. Ultimately, valuation models and metrics are only an approximation of the company’s intrinsic worth at a snapshot in time, and that snapshot can change quickly when the business keeps executing.

Themes where there is a structural supply demand shortage.

In these setups, the business does not need perfect macro conditions to grow. Capacity is constrained, demand is persistent, pricing has leverage, and growth becomes incremental by default. In an expensive market, those are the kinds of situations that can still deliver real upside because the fundamentals are mechanically tight.

Top Ideas for 26’

1. Axon (AXON)

Axon is still my favorite asymmetrical set-up for 26’.

Stock discounted ~33% from august highs because investors compressed valuation multiple over a “bookings miss” (13% growth vs expectations) and a GAAP net loss driven by non-cash charges and tariffs.

I addressed the set-up in detail in the Axon deep dive:

“First, a meaningful portion of the bookings softness appears tied to federal budget timing. The threat of a U.S. government shutdown can effectively freeze parts of the federal procurement process, pushing contract signings from Q3 into Q4. That’s a timing issue, not a product demand issue.

Second, management’s tone on the earnings call was notably constructive on Q4 and the longer-term outlook over the next 3–5 years. That matters because the market traded the quarter as if Axon had revealed a growth ceiling. But the data and the tone suggest Q3 was simply short-term turbulence inside a broader platform transition. The multi-year compounding narrative looks intact.”

Thesis 1: The AI Era plan is the margin and ARR unlock

AI Era plan was Axon’s fastest growing product in company history, with about 150 million of bookings in the second quarter. Sell side model 50 percent penetration by 2030 which translates to roughly 400k seats and about 950 million of ARR.

Thesis 2: International is an under-penetrated seat expansion engine

International expansion unlocks a new TAM of 76 billion.

Cloud adoption in Europe is accelerating (tracking about 10 years behind the U.S.). Analysts estimate a $3.7 billion revenue opportunity across 17 European countries alone. Furthermore, international revenue grew 67% year-over-year recently, and the company closed a “9-figure cloud deal” in Europe in October 2025

Thesis 3: The Enterprise Market (Retail & Healthcare)

Axon is aggressively moving beyond law enforcement into the private sector, targeting frontline workers in retail, healthcare, and logistics. Recently, the company launched specific hardware (Workforce and Workforce Mini) designed for private employees to combat theft and workplace violence.

The Enterprise TAM is estimated at $48 billion, which is roughly 20 times the size of the traditional public safety personnel market. Axon recently signed its largest-ever commercial deal with a global logistics company and sees “pent-up demand” from Fortune 500 retailers

2. Applovin (APP)

Applovin is my biggest position throughout the majority of 2025, and I expect this to continue into 2026 given that my core thesis (E-commerce and self-service platform) haven’t fully played out yet.

Early in 2025, the stock got hit by a rolling sequence of short reports that went straight at the company’s credibility rather than quarter to quarter execution. Fuzzy Panda published a short thesis on February 26, 2025, and Muddy Waters followed with its report on March 27, 2025. The accusations include:

Applovin violated platform partner agreements (such as those with Apple and Google) by using unauthorized tracking methods like device fingerprinting to target ads.

Reports accused the company of engaging in manipulative tactics, including “clickjacking” and “backdoor installations” of apps without user consent.

The reports alleged that Applovin misrepresented its AI capabilities and financial growth to investors

In October 2025, Reuters reported that the SEC had been probing AppLovin’s data collection practices, with Bloomberg citing a whistleblower complaint and multiple short seller reports as part of the context.

Looking back, those episodes were noise for one simple reason. The economic reality advertisers care about did not break. Every stock plunge were later proven to be a great opportunity to enter into a compounding cash-printing machine.

The accusations of “fraudulent” or low-quality traffic are contradicted by data from third-party attribution firms. For example, Northbeam reported that for Direct-to-Consumer (DTC) brands, AppLovin’s Return on Ad Spend (ROAS) was 45% higher than Meta’s and 74% higher than TikTok’s. This performance validation from external auditors suggests the ad inventory is high-quality and legitimate.

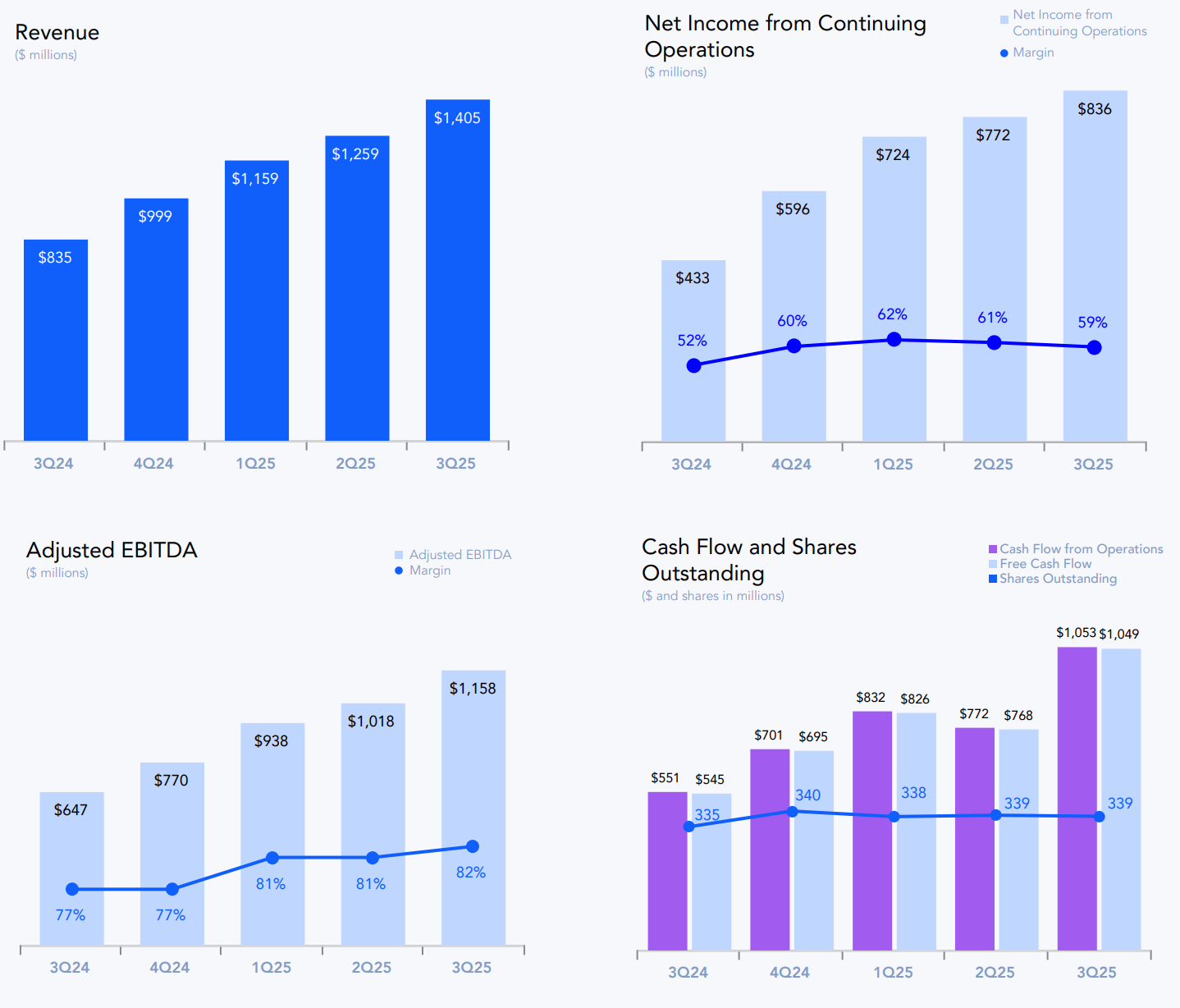

Execution also continued smoothly despite headline noises. In Q3 2025, AppLovin reported 68% year-over-year revenue growth to $1.4 billion and an 82% Adjusted EBITDA margin, argubly the best finnacial profile among broader SaaS names.

The bullish case argues that AppLovin has a reliable core gaming business that can grow 20-30% YoY solely given model improvements, and the company is in the early stages of a massive total addressable market (TAM) expansion via its new self-service platform for web advertisers.

The E-Commerce and Self-serve Opportunity

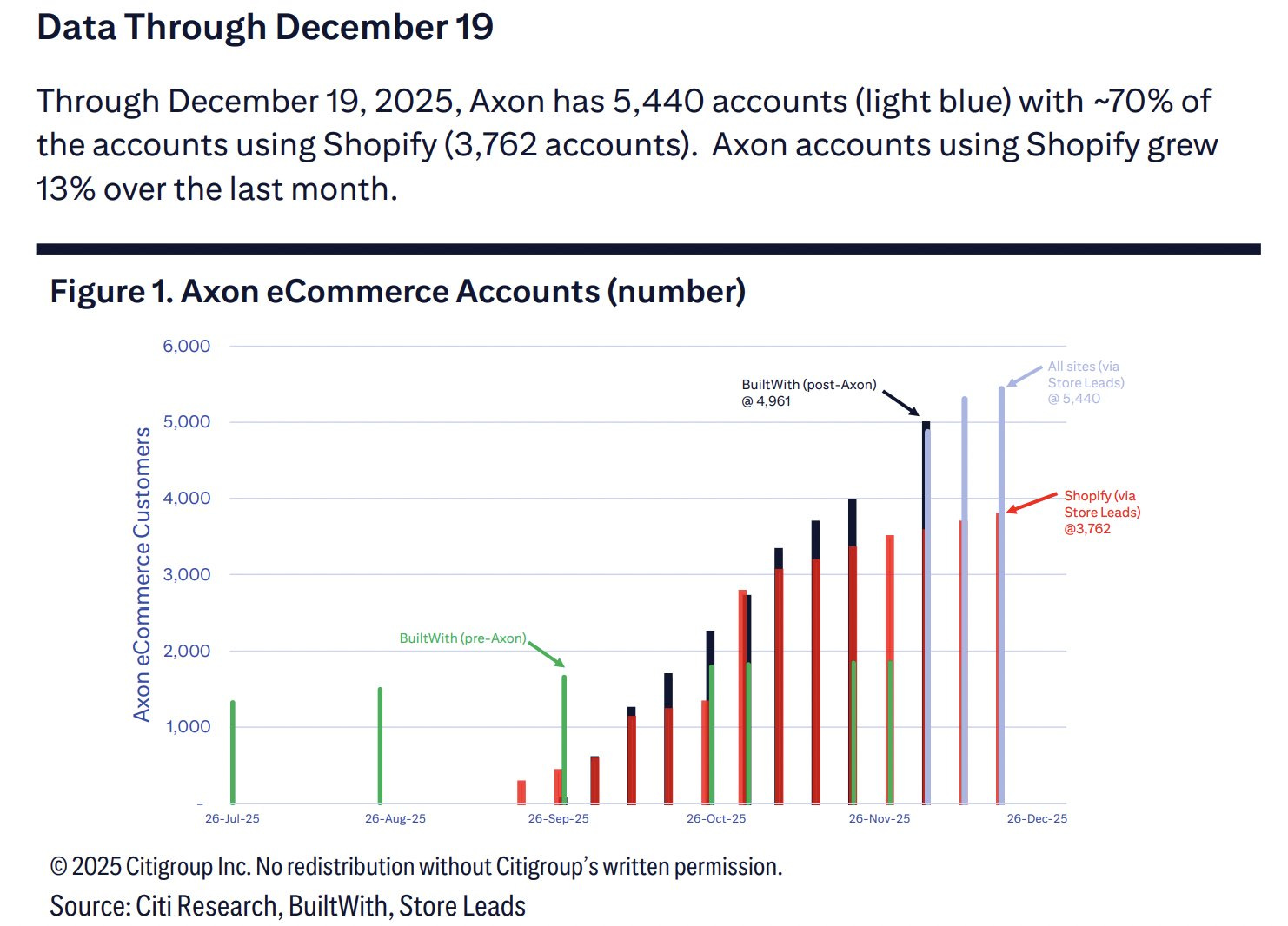

In October 2025, AppLovin launched Axon Ads Manager, a self-service platform for e-commerce and web advertisers. Early data showed spend on this platform growing roughly 50% week-over-week immediately post-launch. AppLovin is monetizing a massive, static base of over 1 billion daily active users (DAUs) who are currently “bombarded” with gaming ads. By injecting e-commerce ads into this stream, AppLovin improves user experience (variety) and increases conversion rates without needing to find new users. Management targets e-commerce contributing significantly to revenue growth in 2026 as the platform opens globally.

Recent E-Commerce progress checks from Citi were also notably positive.

The Q4 guidance Applovin released on Q3 earnings only reflects continued model improvements and typical holiday seasonality, but excluded potential incremental revenue from new advertisers onboarding via the referral program. If onboarding velocity holds, it implies a materially increased likelihood of outperformance next quarter and forward.

Before AppLovin’s breakout in 2024, the consensus view was that adtech was a red ocean and the winners were already decided. Then AppLovin showed up and took share anyway. It did it by providing measurably better ROAS for advertisers compared to competitors, and that is why it was able to pressure incumbents like Unity’s Vector and Google’s AdMob. If that same playbook translates into web based ecommerce at scale, the valuation conversation changes quickly. The upside is that the market has to reframe AppLovin as a much larger platform with a much larger budget pool.

3. Amazon (Amazon)

Amazon is one of the few mega caps where the fundamental story has improved meaningfully, while the stock has spent a lot of the last year being treated like a “funding source” for higher beta AI winners. The setup matters because 2026 is not starting with relatively cheap valuation compared to historical episodes.

The market spent two years narrating AWS as an AI laggard and pricing the company accordingly. Their most recent earnings put a dent in that narrative. AWS grew 20 percent year over year to $33.0 billion, while consolidated net sales grew 13 percent to $180.2 billion. A few weeks later, OpenAI signed a seven year, $38 billion cloud services deal with AWS, which is about as clean of an external validation signal as you can get in the current compute constrained world.

The most important point is that AWS re-accelerated. At the same time, the OpenAI partnership formalized the idea that the next two years of cloud growth may be limited less by customers and more by how fast providers can stand up power, racks, and GPUs. Thankfully, Amazon is expanding capacity faster than ever before.

Full thesis:

4. Rubrik (RBRK)

Rubrik sold off significantly after its fiscal second quarter 2026 print despite results that were objectively strong. Subscription ARR grew to about 1.25 billion, and the company posted meaningful outperformance on operating metrics including free cash flow, yet the stock still traded down because expectations had moved ahead of the quarter.

Going into the fiscal third quarter print, Rubrik was already carrying a lot of skepticism in the price. The stock had been treated like a high growth security name with a fragile multiple, so sentiment was leaning negative and the bar was not demanding. When the company delivered a strong quarter where EPS flipped positive, the stock popped more than 26% as investors were forced to reprice fundamentals that were clearly better than the tape had implied.

Then the tape reversed: -17% since earnings high.

The pressure lined up with two flow driven forces. First, Lightspeed began an in kind distribution of more than three million shares starting December 11, creating an incremental supply overhang. Second, the whole high growth security complex sold off more than five percent in the same window, with names like NET, CRWD, and ZS dragging sentiment lower. In that context, a stock can trade back toward pre earnings levels even after a strong beat and raise, simply because supply and risk off positioning overwhelm fundamentals in the near term.

If the business is still tracking a mid 30s ARR trajectory and free cash flow is inflecting, a pullback driven by distribution and sector derisking is not a thesis change.

Deep dive:

5. Nvidia

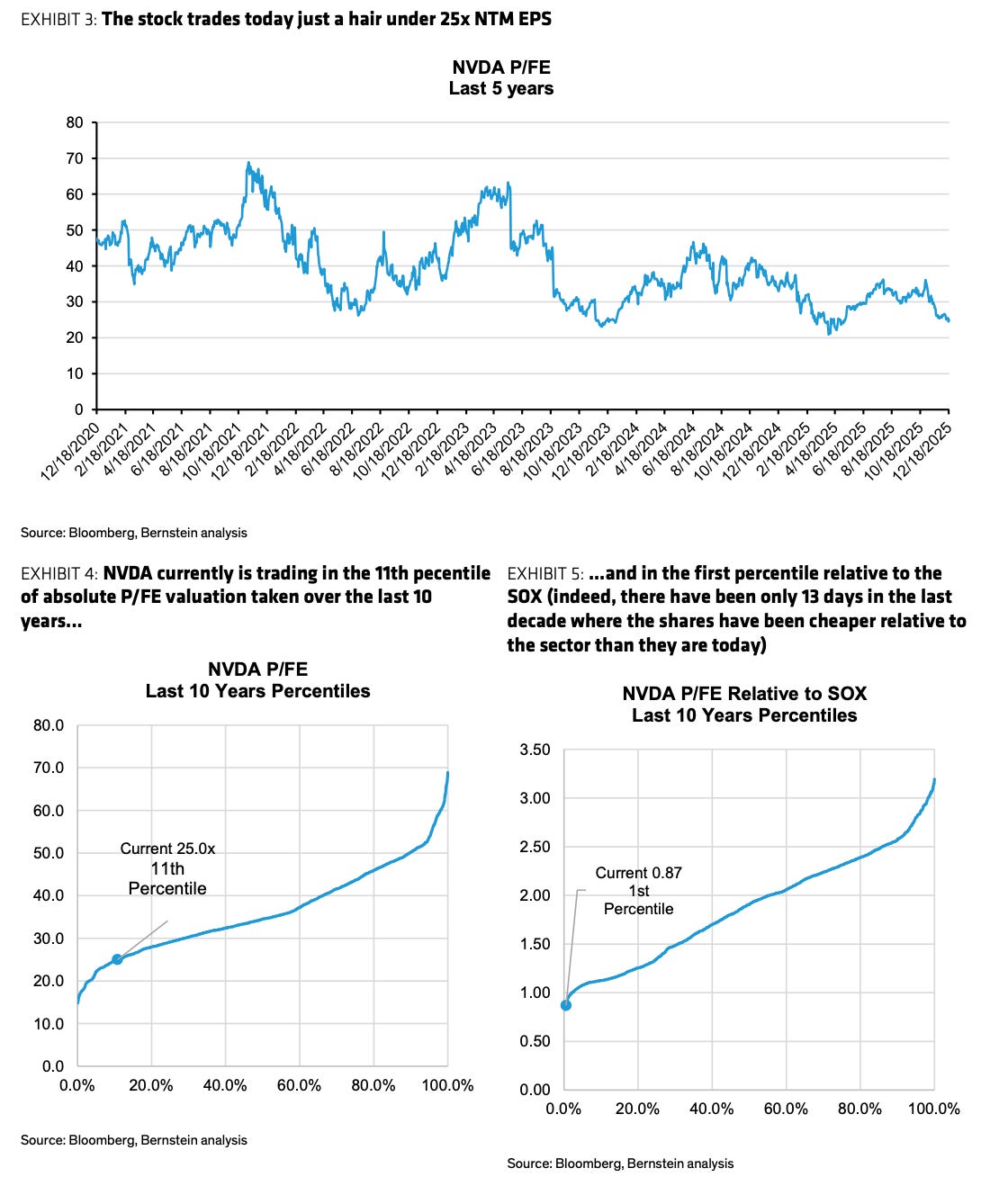

Nvidia enters 2026 with the tape in a very different place than the narrative. After a strong run earlier in the year, the stock has recently lagged the broader semiconductor complex, falling roughly 13 percent versus the SOX. The pullback were tied to renewed investor anxiety around AI capex durability and a rotation away from the most crowded winners, even as underlying demand signals remain constructive.

Bernstein highlights that Nvidia now trades at a decade low relative valuation versus the SOX, in the first percentile on their history, and notes that the stock has only been cheaper on their framework for 13 days over the last ten years.

I remain convinced that Nvidia is among the best way to play AI compute. In the near term, catalysts such as CES / GTC, product cadence, incremental positive headlines with China related approvals and significantly improved Blackwell models in Q1 this year should boost investor confidence over the implied forward revenue trajectory.

6. Optics, Advanced Packaging, and AI power being the key themes to watch

The market is gradually moving from a pure GPU cycle to a full data center systems cycle. In 26, the highest signal areas to watch are the physical layers that sit around the GPU. As clusters scale, performance and delivery cadence get gated by interconnect bandwidth, packaging throughput, and time to power. When a layer of the stack is scarce, it captures outsized economics and becomes the swing factor for both quarterly shipment cadence and multi year capex plans.

1. Advanced Packaging

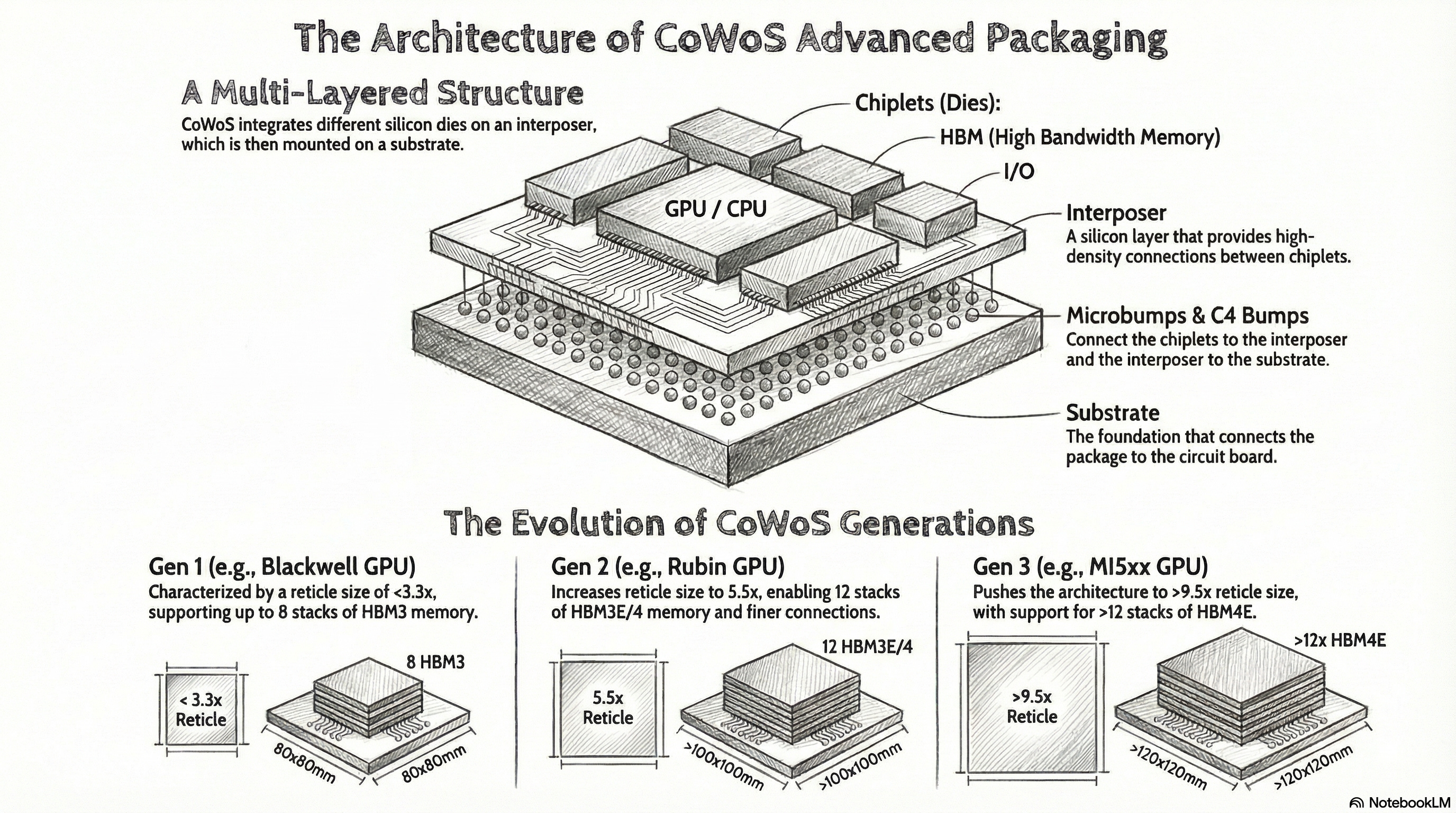

For decades, chips got faster by making transistors smaller (Moore’s Law). Around 2022-2023, this became physically difficult and exponentially expensive. The exponential growth in AI chip performance requirements has mandated a fundamental architectural transition away from relying solely on monolithic die scaling. To keep increasing performance for AI, engineers stopped trying to make one giant, perfect chip. Instead, they started “gluing” smaller, specialized chips together. Advanced packaging, specifically 2.5D and 3D integration platforms, has become the primary vector for realizing necessary performance gains in high-performance computing (HPC) cores, GPUs, and AI ASICs.

Chip-on-Wafer-on-Substrate (CoWoS) is the dominant commercial technology in this space. CoWoS integrates the high-performance logic die (such as a GPU or custom ASIC) with High Bandwidth Memory (HBM) cubes onto a silicon interposer. Here’s a photo of what CoWoS compoenents looks like:

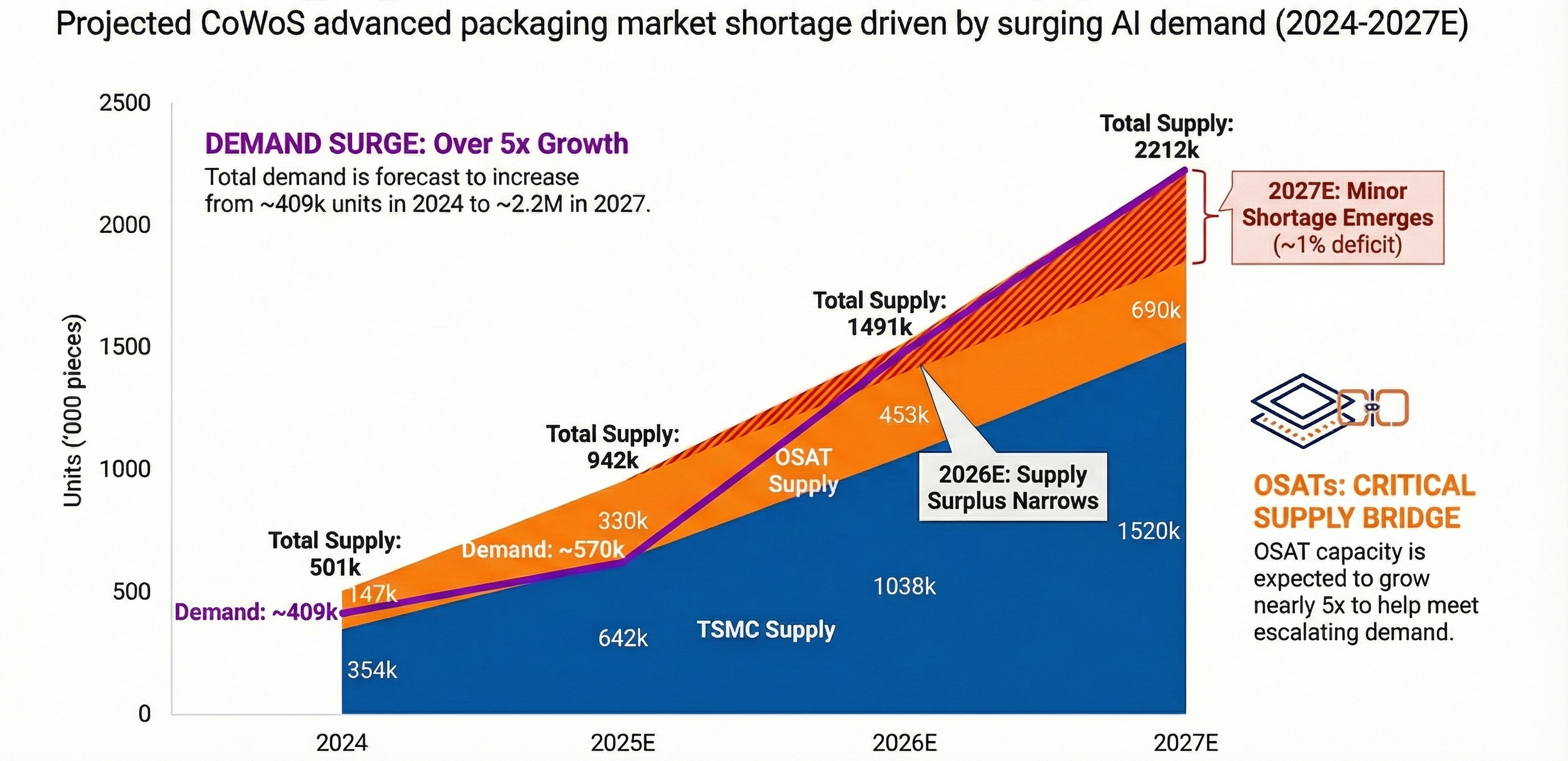

The explosive growth of AI development has created an insatiable appetite for the advanced packaging needed to build powerful processors. Demand is projected to grow at a staggering 70-80% compound annual growth rate (CAGR) from 2024 to 2027.

NVIDIA is the single most critical driver of CoWoS demand, projected to secure a commanding share of this capacity. Forecasts indicate that NVIDIA will book a total of 595,000 CoWoS wafers by 2026, securing approximately 60% of the total global advanced packaging output. In addition, structural demand for advanced packaging is reinforced by major hyperscalers who are committing substantial capital to the development of proprietary, multi-die AI silicon (ASICs). Broadcom, a key ASIC provider and designer, is forecast to acquire 150,000 CoWoS wafers (15% of total demand). This capacity predominantly serves custom chips for massive clients, including 90,000 wafers allocated for Google’s TPUs and 50,000 for Meta. AMD, another major user of the technology, is forecast to acquire 105,000 CoWoS wafers (11% of total demand) for its MI355 and MI400 series chips, primarily sourced through TSMC. Additionally, major cloud providers like Amazon Web Services (AWS) have booked 50,000 wafers through partners such as Alchip, further intensifying the competition for scarce capacity.

Despite significant capacity expansion by industry leader TSMC, a supply shortage is projected to widen to 30% in the next 18-36 months.To maximize its output of high-value, front-end chips, TSMC is increasingly outsourcing lower-margin but essential back-end processes. This strategic outsourcing is the primary catalyst for the growth of the OSAT providers, creating distinct opportunities in on-substrate (oS) assembly line. These companies have readily available capacity to capture overflow demand and are set to capture first-source CoWoS opportunities, including NVIDIA’s GB10, Vera, and B30, as well as Broadcom’s TPU ASICs in 2026.

Key tickers: $AMKR,$ASX

2. Time-To-Power

After decades of relatively flat demand, the United States is entering a structural upcycle driven by manufacturing returning onshore and data centers scaling at a pace the grid was not built for. US electricity consumption is expected to grow around 2.6 percent per year over the next decade, while data center demand is accelerating materially faster.

AI and data centers drive the majority of near term incremental load, and projections that data center electricity consumption reaches roughly 824,000 GWh by 2030 and about 1,050,000 GWh by 2035. Based on MS estimates, US will likely face a 49 GW power deficit by 2028 driven largely by data center and AI load growth outpacing grid additions.

The problem is that the industry is not only “short in power” but more importantly “short in quickly deployable power”. When a data center cannot secure firm electricity on schedule, delayed enterprise migrations, lower utilization of already-installed compute, and missed AI workloads can cost more than $1.25 billion in deferred revenue.

Key tickers: $BE, $GEV

3. Optics & Photonics

For decades, copper wiring has served as the nervous system of computing, but it can no longer efficiently handle the massive, parallel data flows required between today’s high-performance processors. For context, a single server rack in an AI data center might contain up to two miles of copper cables connecting hundreds of chips, all of which are becoming performance-limiting bottlenecks. The physical constraints of sending data via electrons over copper wires are now a primary obstacle to scaling AI. This electrical signaling is now generating too much heat, consuming too much power, and losing signal integrity over the short distances inside a server rack, threatening to stall the very progress of AI it is meant to support.

To break through the copper wall, the industry is turning to technologies that transmit data using light (photons) instead of electricity (electrons). This transition is enabled by a suite of innovations that are moving optics from long-haul cables directly onto the silicon chips that power AI.

Co-Packaged Optics (CPO) represents a major architectural shift. It involves integrating optical engines directly adjacent to the main processing chips on the same package, dramatically shortening the electrical traces data must travel. This proximity unlocks massive gains in performance and efficiency compared to traditional pluggable optics that sit on a server’s faceplate. In 2025, key players like Cisco and NVIDIA began field trials of 51.2T CPO switches, signaling the technology’s readiness for deployment.

AI infrastructure is increasing optical intensity. As clusters scale, you need more high-speed links, and link speeds are moving up the curve (400G to 800G and toward 1.6T). Even if unit pricing per bit declines over time, total optical dollars can grow because the number of links and the bandwidth per link are rising faster.

Key tickers: $AXTI, $LITE, $SMTC, $ COHR

Conclusion

Before wrapping up, I want to express sincere gratitude to both my free subscribers and paid subscribers. Your support has been what motivated me to keep writing articles like this.

To my paid subscribers specifically: Your support has been consistent and generous, especially when I’ve published a meaningful amount of free content. I do not take your support for granted. The ability to research deeply, write thoughtfully, and keep improving the work is directly enabled by the people who chose to back it.

As a small way to give back, I’m going to share my full portfolio disclosure and specific trading plan at this current moment. This will include my current holdings by name and approximate position sizing. My intention is to be as transparent as possible so you can see how I translate research into actual capital allocation, how concentrated (or diversified) I am, and which ideas I believe offer the most attractive risk/reward over my time horizon.