IDEA | Amazon (AMZN): Several Ways to Win

A fundamental narrative shift from AI-Laggard to AI-Winner: Structural cloud re-acceleration, advertising opportunity, and retail optimization drive asymmetric upside

Over the trailing 12 months, market sentiment surrounding Amazon (NYSE: AMZN) has been weighed down by the growing skepticism regarding its status as a potential ‘AI laggard,’ with investors increasingly concerned that Amazon is conceding its cloud leadership to Microsoft Azure, Google Cloud Platform (GCP), and Oracle Cloud Infrastructure (OCI).

This sentiment was compounded by a deceleration in Amazon Web Services (AWS) revenue growth, which began in 2H22 and served as the primary catalyst for the stock’s de-rating. AWS shifted from being a consistently high growth/margin business (historically 30% growth and 30% margin) to one exhibiting top-line growth only in the teens (13% in 2023 and 19% in 2024). The deceleration in growth within AWS—a critical segment generating 56% of total operating income—has precipitated a material compression in valuation. Consequently, the company’s EV/EBITDA multiple has contracted from historical premiums exceeding 20x to recent levels of approximately 12x. For the majority of 2025, Amazon shares functioned effectively as a “funding short” for the broader AI trade, where the stock became a reliable source of liquidity for institutional investors rotating capital into higher-beta “pure play” infrastructure stocks.

Amazon’s EV to EBITDA (May 26, 2021 - Nov 19, 2025)

Following Amazon’s Q3 earnings, however, I believe AMZN now represents a highly asymmetric risk/reward opportunity, driven by three distinct but reinforcing flywheels: the resurgence of AWS growth, retail cost-to-serve optimization, and high-margin advertising opportunity. This confirmed inflection in cloud trajectory serves as the definitive catalyst for a valuation reset. Consequently, I anticipate a structural mean-reversion in the EV/EBITDA multiple toward historical averages over the next 12–36 months, fueled by the compounding effects of AI infrastructure deployment and retail operating leverage.

Section 1: The AWS Re-Acceleration

For nearly two years, the valuation ceiling on Amazon stock was dictated by the deceleration of AWS revenue growth, which trough in the low teens during 2023 as enterprise customers optimized spend. The third quarter of 2025 marked a significant reversal of this trend. AWS reported revenue of $33.0 billion, representing a 20.2% year-over-year increase.

This performance exceeded consensus estimates by approximately 220 basis points and marked the fastest growth rate for the segment in 11 quarters.

For nearly two years, the valuation ceiling on Amazon stock was dictated by the deceleration of AWS revenue growth, which trough in the low teens during 2023 as enterprise customers optimized spend. The third quarter of 2025 marked a significant reversal of this trend. AWS reported revenue of $33.0 billion, representing ~56% of operating income and a 20.2% YoY increase. This performance exceeded consensus estimates by approximately 220 basis points and marked the fastest growth rate for the segment in 11 quarters.

It is crucial to distinguish that the quality of this revenue expansion indicates active market share capture. Sequential dollar growth for AWS reached $2.1 billion in Q3 2025, materially outpacing Microsoft Azure’s estimated $1.7 billion sequential add. This is the first time since Q3 2022 that AWS has widened the sequential dollar growth gap against its primary competitor, signaling a reassertion of dominance in the expanding Total Addressable Market (TAM) for cloud infrastructure. This metric effectively rebuts the narrative of perpetual share loss in the increasingly competitive cloud space.

Currently, AWS revenue growth is gated by supply constraints rather than demand limitations. It is a fundamentally optimistic indicator for future quarters as massive capacity investments come online. Management commentary explicitly highlights that revenue growth would have been higher in 2025 were it not for near-term capacity limitations, a dynamic mirrored by peers such as Microsoft Azure, suggesting a sector-wide super-cycle of demand.

To resolve the supply-demand mismatch, Amazon has committed on the most aggressive capital expenditure cycle in its corporate history. The company added over 3.8 gigawatts (GW) of power capacity over the past year—a figure that exceeds the total capacity additions of several competitors combined—and expects to add at least 1 GW more in Q4 2025.

The strategic roadmap is explicit: Amazon has doubled its total capacity since 2022 and plans to double it again by 2027. While capital intensity is rising—with 2025 Capex projected at $125 billion and 2026 expected to climb further to ~$162 billion—historical correlations suggest this is a precursor to revenue expansion.

Goldman Sachs analysis highlights a critical historical precedent: during the period from 2022 to 2025, when AWS capacity doubled, segment revenue increased by 60%. Current models project AWS revenue to increase by approximately 45% between 2025 and 2027 as capacity doubles again. Given that AI workloads are generally more compute-intensive and higher-priced than traditional storage/compute workloads, there is a strong argument that the revenue yield per gigawatt of new capacity could exceed historical norms, providing upside to the 45% growth estimate.

1.1 The OpenAI Strategic Partnership

In a development that fundamentally alters the competitive landscape of the cloud industry, Amazon announced a multi-year strategic partnership with OpenAI in November 2025. This agreement represents a committed spend of $38 billion over seven years, under which OpenAI will utilize AWS infrastructure for its core artificial intelligence workloads.

Key Deal Parameters:

Financial Magnitude: $38 Billion cumulative commitment, with workloads commencing immediately.

Deployment Timeline: Full capacity deployment is targeted by year-end 2026, with contractual provisions to expand further into 2027 and beyond.

Infrastructure Specifications: OpenAI will utilize Amazon EC2 UltraServers, leveraging clusters of hundreds of thousands of Nvidia GPUs (specifically the GB200 and GB300 series), scalable to tens of millions of CPUs.

Revenue Impact: Analysts project this deal alone will contribute approximately 3 percentage points to AWS revenue growth by 2027. When combined with the existing Anthropic partnership, Amazon’s AI-specific revenue contribution is expected to exit 2026 at an annualized run rate exceeding $20 billion.

The strategic significance of the OpenAI deal to AWS is much more than pure financial contribution. Previously, the market perception was that OpenAI was inextricably linked to Microsoft Azure, creating a closed ecosystem. By securing this partnership, AWS has effectively broken the exclusivity narrative, validating its strategy to function as a neutral, high-performance Cloud Service Platform (CSP) capable of hosting the diverse workloads of the industry’s fiercest competitors.

Amazon now holds deep, pivotal infrastructure partnerships with the two leading private AI model entities globally: Anthropic and OpenAI. This diversification effectively de-risks the AWS investment thesis from a model-specific perspective. Regardless of whether GPT-5, Claude 4, or another foundational model captures the most market share, AWS provides the underlying compute utility, monetizing the aggregate growth of the sector.

1.2 Project Rainier: The Anthropic Mega-Cluster

While the OpenAI partnership relies heavily on third-party Nvidia GPUs (GB200/GB300), Amazon’s long-term margin preservation strategy hinges on its proprietary silicon stack. “Project Rainier” represents the massive, tangible realization of this strategy. This initiative involves a geographically distributed AI compute cluster spanning multiple data centers, specifically brought online to support Anthropic’s development of Claude and subsequent foundation models.

Project Rainier Operational Metrics:

Current Scale: Equipped with nearly 500,000 Trainium2 chips as of late 2025.

Expansion Trajectory: The cluster is expected to scale to over 1 million Trainium2 chips by year-end 2025, representing one of the largest single-architecture AI clusters in the world.

Utilization: Anthropic is actively utilizing this cluster for both model training and deployment. This serves as a massive “proof of concept” for the broader enterprise market, demonstrating that frontier models can be successfully trained on non-Nvidia silicon.

The market adoption of Trainium2—Amazon’s second-generation machine learning training chip—is accelerating at a rate that confirms the viability of Amazon’s vertical integration. Revenue associated with Trainium2 grew 150% quarter-over-quarter in Q3 2025, and the hardware is reportedly fully subscribed.

This demand signal is critical for the long-term profitability of AWS. Reselling Nvidia GPUs carries a “gross margin tax” due to Nvidia’s pricing power. By migrating workloads to Trainium, AWS can offer lower prices to customers (price-performance advantage) while retaining higher gross margins for itself. This creates a competitive moat against cloud competitors like Azure and OCI, who may be more dependent on third-party silicon for their AI offerings.

Looking ahead, the innovation cycle remains rapid. Trainium3 is slated for preview by year-end 2025, with broader commercial rollout in early 2026. Trainium3 is expected to deliver a 40% performance improvement over Trainium2, further incentivizing customers to migrate away from the CUDA ecosystem for specific workloads.

Section 2: Retail Business Resilience

While the cloud narrative dominates the headlines, Amazon’s core retail business is undergoing a quiet but powerful efficiency revolution that is driving operating income higher.

2.1 Operational Efficiency and Regionalization

Amazon’s strategic pivot from a national fulfillment network to a regionalized node structure continues to yield compounding dividends. The company has reduced U.S. inbound lead times by nearly four days year-over-year. This speed metric is the primary driver of retail economics: faster delivery increases conversion rates (revenue) while simultaneously reducing the “cost to serve” by minimizing package travel distance and “touches.”

Operating margins in the North America segment reached 5.9% in Q3. However, when normalized to exclude one-time charges related to the FTC settlement ($2.5 billion) and severance costs ($1.8 billion), the underlying operating margin is estimated between 6.9% and 8.0%. This demonstrates a robust upward trajectory toward double-digit margins. With over 1 million robots now deployed across the fulfillment network to automate picking and sorting, management indicates that retail operating income can sustain ~20% growth going forward, outpacing revenue growth.

2.2 Grocery and Essentials

The retail strategy is increasingly anchored by “Everyday Essentials” and Grocery, a segment generating over $100 billion in Gross Merchandise Sales (GMS) and growing nearly 2x faster than the core retail business over the past 12 months. This volume effectively positions Amazon as a top-three U.S. grocer.

Management is leveraging this momentum to drive platform habituation, as they explicitly noted that grocery customers exhibit 2x the site visit frequency of non-grocery shoppers. To sustain this high-velocity loop, the company is densifying its logistics network by expanding perishable delivery to over 2,300 cities and introducing rapid 3-hour delivery windows. while simultaneously evolving its physical presence with new ‘Daily Shop’ formats. Furthermore, the company is testing a smaller urban “Daily Shop” concept designed to capture mid-week top-up shopping, distinct from the weekly stock-up trip. This omnichannel approach drove Physical Stores revenue to $5.6 billion (+7% Y/Y) in Q3.

2.3 Rural Network Expansion

To unlock the next leg of domestic retail growth, Amazon has committed over $4 billion to expand its delivery network into rural America. This investment has already increased the number of rural communities eligible for same-day and next-day delivery by 60%. By insourcing the “last mile” in these lower-density areas, Amazon reduces its reliance on third-party carriers (UPS/USPS), capturing the shipping margin and bringing millions of new households into the Prime ecosystem’s high-frequency loop.

Section 3: Agentic Commerce

Beyond infrastructure, Amazon is aggressively colonizing the application layer of AI, focusing on tools that drive developer lock-in and consumer transaction velocity.

3.1 The Rufus Multiplier

Amazon is deploying Generative AI directly into the retail user interface to reduce friction and increase conversion. “Rufus,” the AI-powered shopping assistant, has achieved rapid scale, boasting 250 million active shoppers and facilitating $10 billion in annualized sales volume.

The metrics surrounding Rufus indicate a profound shift in consumer behavior. Monthly Active Users (MAU) for the tool grew 140% year-over-year, with interaction volume up 210%. Crucially, data shows that shoppers using Rufus have a 60% higher probability of completing a purchase compared to those who do not.1 This suggests that Rufus is not merely a chatbot but a high-velocity conversion engine that directly translates AI investment into Gross Merchandise Volume (GMV).

3.2 Developer Tools on Coding Workflow

To secure the loyalty of the next generation of developers, Amazon launched “Kiro,” an AI-native Integrated Development Environment (IDE). The preview version of Kiro attracted over 100,000 developers within days of launch, a number that has since doubled.

Furthermore, the “AgentCore” Software Development Kit (SDK)—a toolkit for building AI agents on AWS—has surpassed 1 million downloads.1 In the enterprise migration space, the “Transform” agent has saved customers over 70,000 hours of manual labor in migration tasks year-to-date. Within the contact center vertical, “Amazon Connect” has utilized these AI capabilities to surpass $1 billion in annualized revenue. These tools create a sticky ecosystem where developers build, deploy, and manage AI applications entirely within the AWS environment, increasing switching costs and reducing churn.

3.3 The Evolution of Alexa

The “Alexa+” initiative represents the monetization of Amazon’s ambient computing footprint. User engagement data indicates that on Fire TV devices, users interact with Alexa+ 2.5x more frequently than the classic version. More importantly for commerce, users are 4x more likely to engage in photo interactions and, critically, 4x more likely to complete a shopping transaction via voice. This suggests that upgrading the massive installed base of Echo/Fire TV devices with LLM capabilities could unlock a new vector of high-margin voice commerce.

Section 4: Advertising

Advertising remains the potent economic engine funding Amazon’s retail investments and bolstering consolidated margins. Revenue grew 24% year-over-year in Q3 to $17.7 billion, accelerating from prior periods.

4.1 Inventory Expansion

The growth in advertising is structural, driven by the opening of new inventory sources. The introduction of advertisements into Prime Video has created a massive new supply of high-value impressions, with upfront commitments for 2025-2026 exceeding management expectations. Additionally, the refinement of the Amazon DSP (Demand Side Platform) and the recent launch of Real-Time Bidding (RTB) capabilities have allowed Amazon to monetize off-site traffic more effectively.

The maturation of the Amazon DSP and Ad Tech stack has unlocked off-site monetization, utilizing new infrastructure ‘pipes’ to access inventory on platforms like Netflix, Spotify, and Roku. With Live Sports driving strong 2026 upfront commitments, the segment is on a trajectory to reach ~$95.5 billion in sales by 2027.

4.2 The Clean Room Advantage

A key differentiator is the “Amazon Marketing Cloud” (AMC), which allows advertisers to utilize clean rooms to match their first-party data with Amazon’s purchase data in a privacy-compliant manner. This capability is driving adoption among non-endemic advertisers (e.g., automotive, financial services) who do not sell products directly on Amazon but covet its audience data.

Assuming a ~55% operating margin for advertising (conservative relative to digital ad peers), this segment contributed nearly $10 billion in operating profit in the quarter alone. The ability to leverage first-party retail data to “close the loop” on ad attribution gives Amazon a structural advantage over competitors like Meta and Google, ensuring that this high-margin revenue stream will continue to compound at a rate roughly double that of the core retail business.

Section 5: Financial Analysis and Valuation Framework

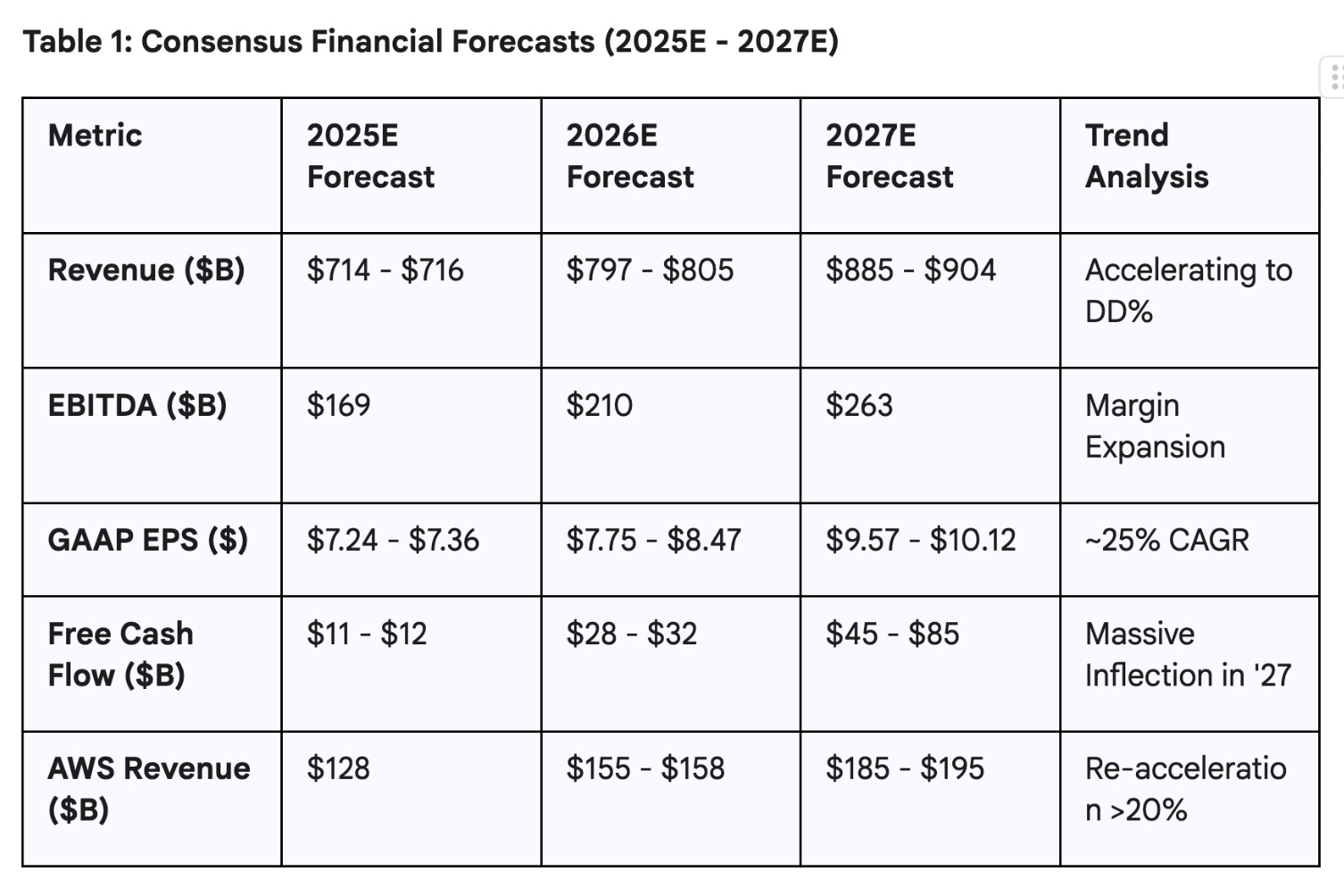

The consensus view anticipates accelerating revenue growth and expanding profitability through 2027.

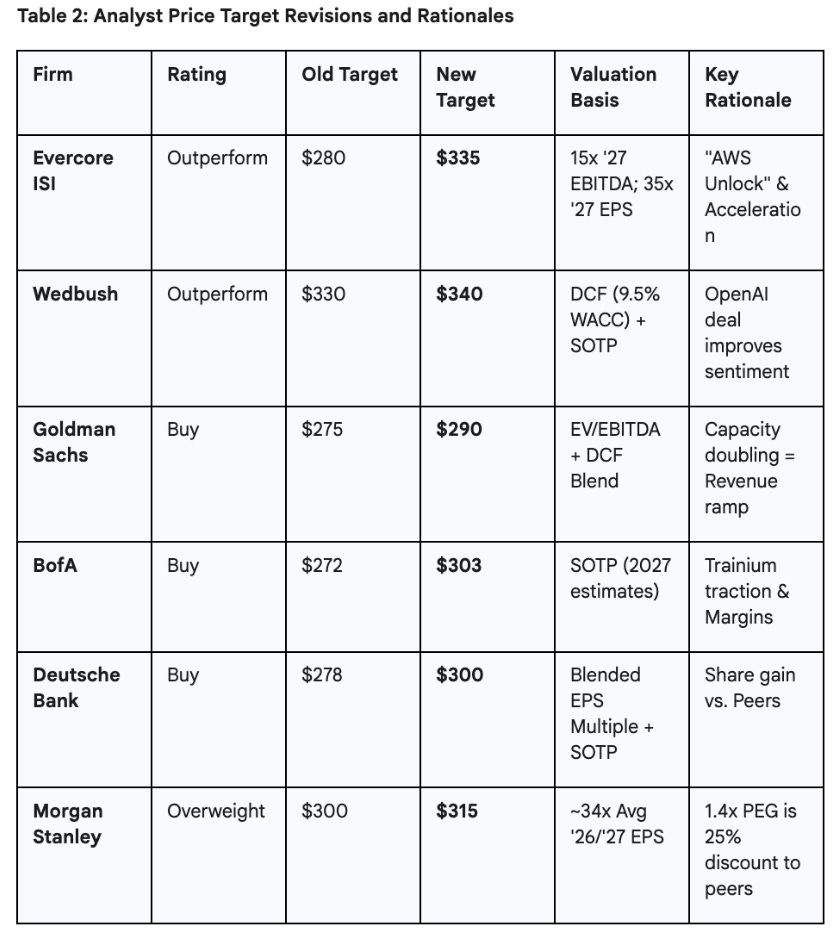

5.1 Estimate Revisions

5.2 Capex

A critical component of the financial model is the trajectory of Free Cash Flow (FCF). FCF is currently pressured by the massive increase in Capital Expenditures (Capex), projected to hit $125 billion in 2025 and rising to $162 billion in 2026.

However, this spend is likely success-based. The unprecedented build-out of data centers (doubling capacity) and procurement of silicon (Nvidia + Trainium) is a direct response to the backlog doubling and secured commitments like the OpenAI deal. While FCF yields may appear low temporarily (0.5% in 2025), the projected inflection in 2026/2027 (rising to ~$45B-$85B) suggests that the current investment cycle will yield substantial cash returns once the infrastructure is deployed and utilization ramps. The “cash conversion cycle” of this Capex is expected to be rapid given the existing supply-demand imbalance.

5.3 Valuation Methodology: Sum-of-the-Parts (SOTP)

Given the distinct economic profiles of Amazon’s business lines, a Sum-of-the-Parts (SOTP) analysis provides the most accurate assessment of intrinsic value.

AWS: Valued at a premium multiple (roughly 8x-10x 2027E Sales or ~25x EBITDA) due to its re-acceleration, backlog strength, and strategic AI positioning. At 44% of the total implied value, AWS is the primary driver.

Advertising: Valued as a high-growth digital media asset (comparable to Meta/Alphabet), commanding ~9x-13x Sales due to its superior margin profile and first-party data advantage.

Retail (1P & 3P): Valued at a standard retail/marketplace multiple (1.0x-2.5x Sales), reflecting lower margins but immense scale and cash flow generation.

Section 6: Risks and Mitigations

Macroeconomic & Consumer Spending Risk: A broader economic slowdown—whether cyclical or triggered by labor market disruptions from widespread AI automation—could severely pressure discretionary e-commerce demand. If transaction volumes contract materially, Amazon’s massive, high-fixed-cost logistics network faces the risk of negative operating leverage, which would erode the recent retail margin gains.

Mitigation: Amazon’s internal application of AI acts as a hedge against lower top-line volumes. By deploying over 1 million robots and utilizing AI to minimize “cost-to-serve” (regionalization), the retail business has structurally lowered its breakeven point to sustain profitability even in a downturn. Furthermore, the strategic pivot toward “Everyday Essentials” (grocery and consumables) creates a defensive, counter-cyclical revenue floor that is less sensitive to disposable income shocks.

Capital Intensity Risk: The projection of doubling capacity by 2027 implies astronomical Capex. If AI demand proves to be a bubble or materially slows, Amazon faces the risk of underutilized assets and significant depreciation headwinds that could compress AWS operating margins.

Mitigation: The backlog is contractually committed (e.g., OpenAI’s 7-year deal), and AWS is designing flexible infrastructure that can be repurposed for general compute if AI demand fluctuates.

Regulatory Risk: The FTC lawsuit regarding antitrust violations and potential regulatory backlash against “Big Tech” dominance remain an overhang. The Q3 earnings were already impacted by a $2.5 billion legal settlement.

Mitigation: The partnership model (hosting OpenAI and Anthropic rather than acquiring them outright) may offer a more defensible regulatory posture than the vertically integrated models of competitors like Microsoft or Google.

Competition: Microsoft Azure and Google Cloud remain formidable competitors with deep pockets.

Mitigation: The OpenAI deal significantly neutralizes Azure’s unique selling proposition (exclusivity), and AWS’s custom silicon (Trainium) puts it ahead of Google in terms of merchant silicon offering scale.

Disclaimer & Important Disclosures

This report is provided for informational and educational purposes only and does not constitute financial, legal, or investment advice. The analysis contained herein reflects the personal opinions of the author as of the date of publication and is subject to change without notice. Nothing in this document should be construed as an offer to sell or a solicitation of an offer to buy any securities or financial instruments.

Forward-Looking Statements: This report contains forward-looking statements regarding future economic conditions, business strategies, and financial estimates (e.g., 2027 revenue projections). These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially from those anticipated. Past performance is not indicative of future results. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.