Macronix (2337.TW) : Hey! Old Memory Is Still Memory

A Story Worth Unwrapping

TLDR

Macronix (2337.TW) is entering a major earnings up-cycle driven by severe supply shortage in MLC NAND , a non-volatile flash memory which can hold data even when it’s not connected to a power source.

Macronix is the last supplier standing in a structurally collapsing MLC NAND supply ecosystem. Every major NAND manufacturer (i.e. Samsung, SK Hynix, Kioxia, and Micron) is exiting MLC production by 2027-2028 as they pivot more toward high margin HBM, advanced DRAM, and higher-density NAND biz. As the major suppliers exit MLC, Macronix is positioned to become the only meaningful remaining supplier of low-capacity eMMC. The supply exit is permanent and irreversible, leaving Macronix as the sole beneficiary.

The MLC market is entering a multi-year supply deficit with the supply-demand gap expected to reach 36% / 47% / 26% in FY26–28E. Pricing is already inflecting as eMMC contract prices rose 100–200% QoQ in 1Q26, with further price increases expected through the year as supply remains tight.

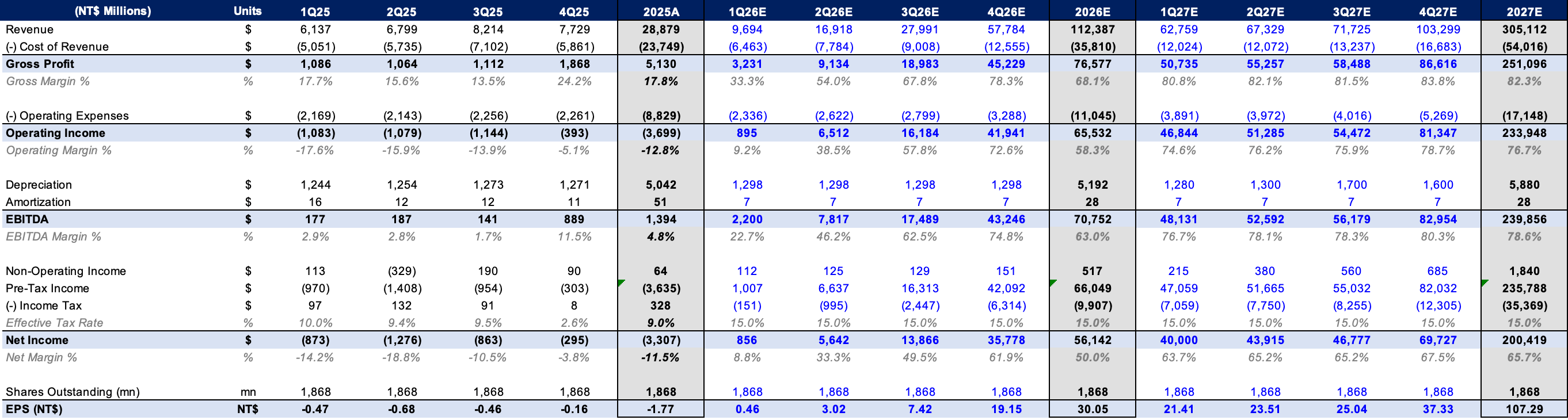

For Macronix, the earnings leverage is substantial. Revenue is projected to expand from NT$28.9bn in FY25 to NT$305.1bn in FY27E, driven primarily by eMMC, which is expected to rise from 3% of revenue to 75% of the mix. EPS inflects from -NT$1.77 in FY25 to NT$107.25 in FY27E. At the current price of NT$160, the stock trades at about 5.3x 2026E EPS or 1.5x 2027E EPS.

Macronix reminds me of Nanya during the DDR4 shortage where the company re-rated to roughly 8–12x FY1E EPS as the market priced in shortage-driven earnings power. In parallel, applying a 10x FY26E multiple to Macronix does not look demanding and supports a NT$300 price target (+87%), with further upside if the eMMC cycle proves more durable than expected.

Understanding The Technology

This part is designed to help less tech-oriented investors to understand Macronix’s revenue segments and technology (i.e. NAND, NOR Flash, eMMC, SLC NAND, ROM, and foundry services..) Feel free to skip to company overview one segment below if comfortable with more technical terminologies

What is memory? Computer memory is a chip that stores data. There are two broad types: volatile memory (Ex. DRAM - data disappears when power is turned off) and non-volatile memory (Ex. Flash - data stays even without power). Macronix makes non-volatile memory only.

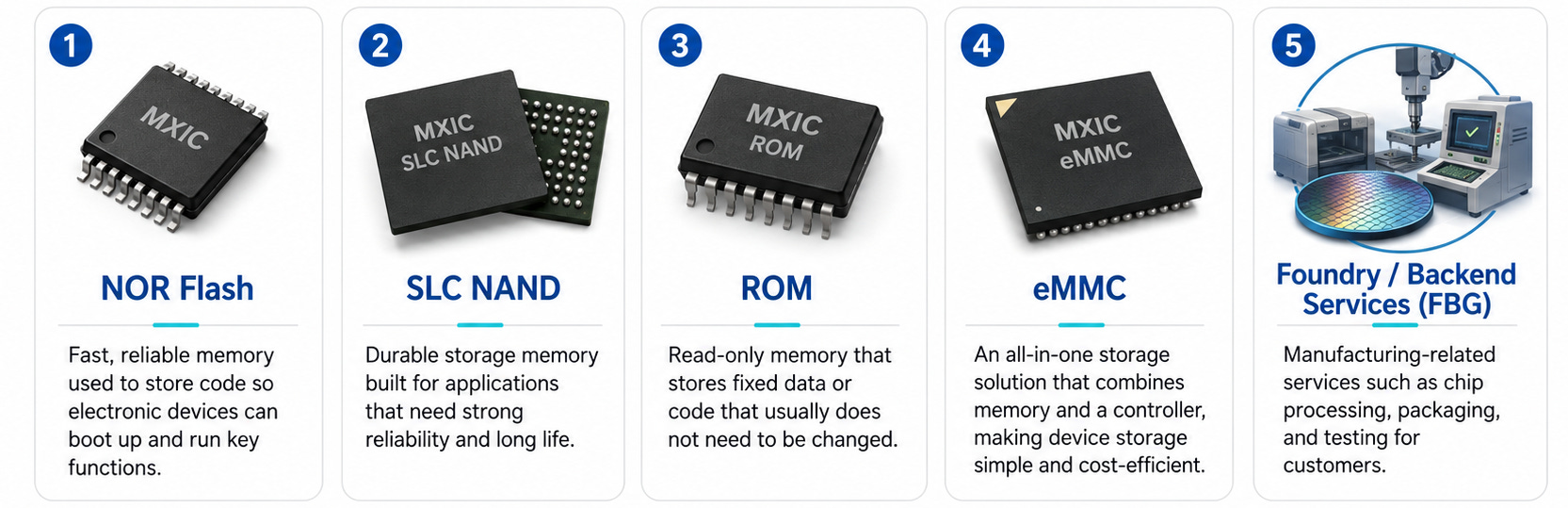

NOR Flash is a type of non-volatile memory designed for fast, random access to individual pieces of data. A processor can read any specific byte of data from a NOR Flash chip almost instantly, without needing to read through other data first.

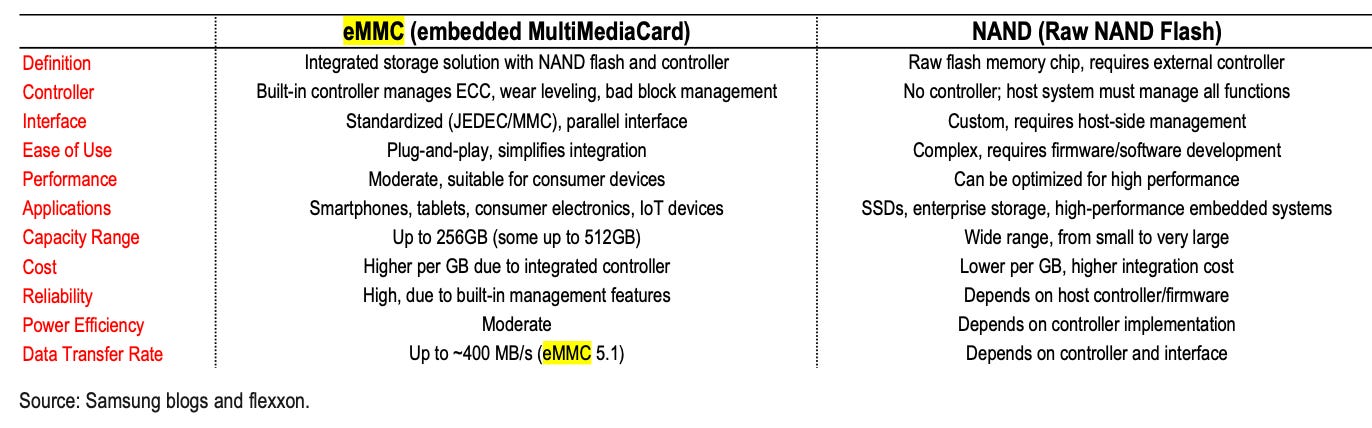

NAND Flash is the other type of non-volatile memory. Unlike NOR, NAND is designed to store large amounts of data efficiently rather than read individual bytes quickly. NAND reads and writes data in blocks (groups of data), which makes it slower for random access but much more space-efficient per chip. The SSDs (solid-state drives) in laptops, phones, and data centers all use NAND Flash. Macronix’s eMMC and SLC NAND products are both types of NAND Flash.

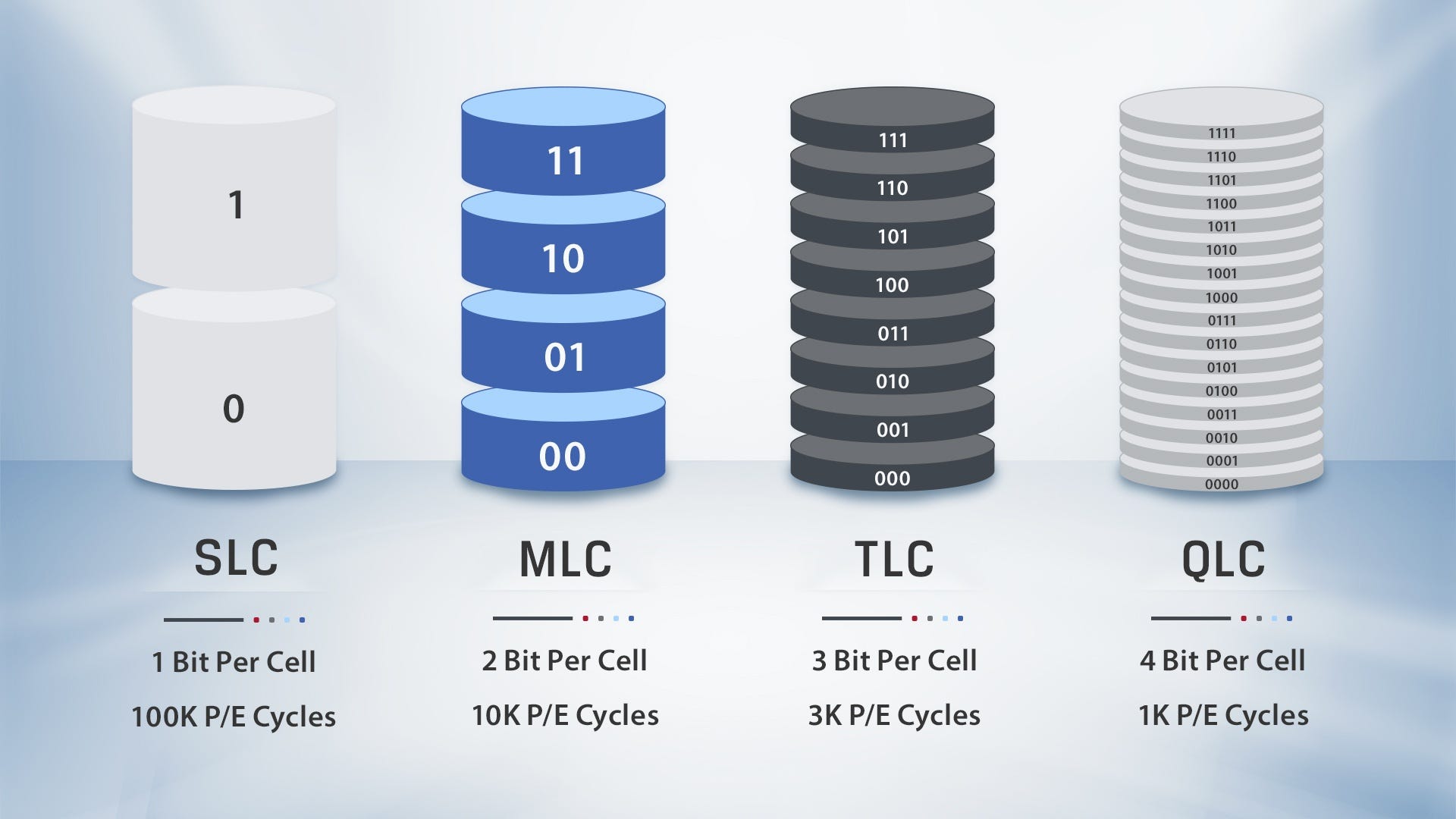

NAND can be produced using 4 different cell structures.

SLC (Single-Level Cell): 1 bit per cell. The cell is either fully charged or fully empty. Because there are only two possible states to distinguish, SLC is the fastest to read and write, the most reliable, and lasts the longest before wearing out. However, it stores the least data per chip, making it expensive per gigabyte. Used in industrial equipment, factory automation, and military/aerospace applications where reliability matters more than cost.

MLC (Multi-Level Cell): 2 bits per cell. The cell has four possible charge levels, representing 00, 01, 10, or 11. More data per chip than SLC, but slower and less durable. Used in eMMC products for consumer electronics, automotive infotainment, and IoT devices.

TLC (Triple-Level Cell): 3 bits per cell. Eight charge levels. The most common type in today’s SSDs for laptops, phones, and data centers. Higher data density makes it the most cost-effective for high-capacity storage. Samsung, SK Hynix, Kioxia, and Micron are all prioritizing TLC (and QLC) production because it generates the most revenue per wafer.

QLC (Quad-Level Cell): 4 bits per cell. Sixteen charge levels. Highest density, lowest cost per gigabyte, but slowest and least durable. Used in some consumer SSDs and data center storage.

Every major NAND manufacturer is moving all of its manufacturing capacity toward TLC and QLC because these store more data per chip and generate more revenue per wafer. MLC lines are being physically shut down and equipment is being repurposed or sold.

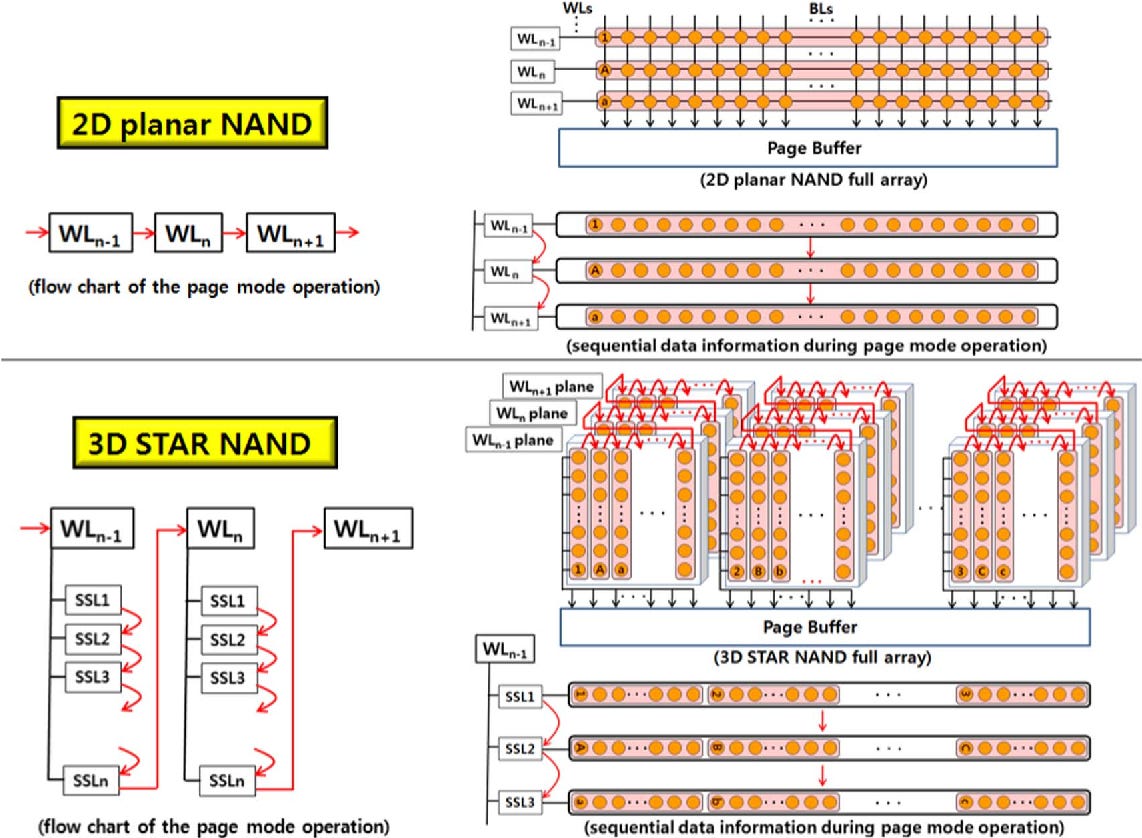

Traditional NAND (called "planar" or "2D") is the earlier form of flash memory where cells are arranged side by side in a single horizontal layer. Although 2D NAND helped establish the foundation for modern flash storage, it reached physical limits as demand for higher capacities grew. It is still used in some lower-cost or legacy applications, but most modern storage has moved toward 3D NAND. In 3D NAND, memory cells are stacked vertically across many layers. This allows manufacturers to increase density without relying only on shrinking the cell size horizontally.

eMMC, or embedded MultiMediaCard, combines NAND memory with a controller in a single package. It combines NAND Flash memory with a built-in controller (a small processor that manages reading, writing, and error correction). eMMC stores the operating system, applications, and user data in devices like smart TVs, set-top boxes, automotive infotainment systems, smartwatches, drones, industrial computers, and networking equipment. Typical eMMC capacity ranges from 4GB to 32GB for the applications Macronix targets. Low-capacity eMMC (≤32GB) is built using MLC or TLC NAND. Macronix is the only company investing to expand MLC/TLC NAND production specifically for eMMC.

Low-capacity eMMC remains important because many customers have designed their systems around specific storage products. In automotive, industrial, drone, networking, and embedded computing applications, changing memory is not a simple purchasing decision. Millions of devices still need MLC-based memory chips (specifically eMMC products in the 4GB-32GB range), and those devices cannot simply switch to TLC chips without redesigning their electronics. This creates demand stickiness even when newer NAND technologies exist. Meanwhile, supply collapses as large NAND suppliers are exiting older MLC-based products at the same time that many customers still need them. The supply shock creates a serious procurement problem and Macronix is the only company poised to solve the gap.

Company Overview

Macronix International Co., Ltd. (2337.TW) is a Taiwanese integrated device manufacturer. It designs its own memory chips, manufactures them in its own semiconductor fabrication plants (fabs), tests and packages them, and sells them directly to electronics companies and through distributors. The company was historically known for NOR Flash, a type of non-volatile memory commonly used to store code that devices need to boot and operate.

Business Deep Dive

The company generates revenue by selling physical memory chips to customers in five product categories: NOR Flash, eMMC, SLC NAND, ROM, and foundry services (FBG). Revenue equals the number of chips shipped multiplied by the price per chip. For volume products like eMMC, the industry tracks this more granularly as bits shipped (measured in gigabits, Gb) multiplied by price per bit ($ per Gb). The company’s cost structure is heavily fixed. The largest cost component is depreciation of fab equipment, followed by raw materials (silicon wafers, chemicals, gases) and labor.

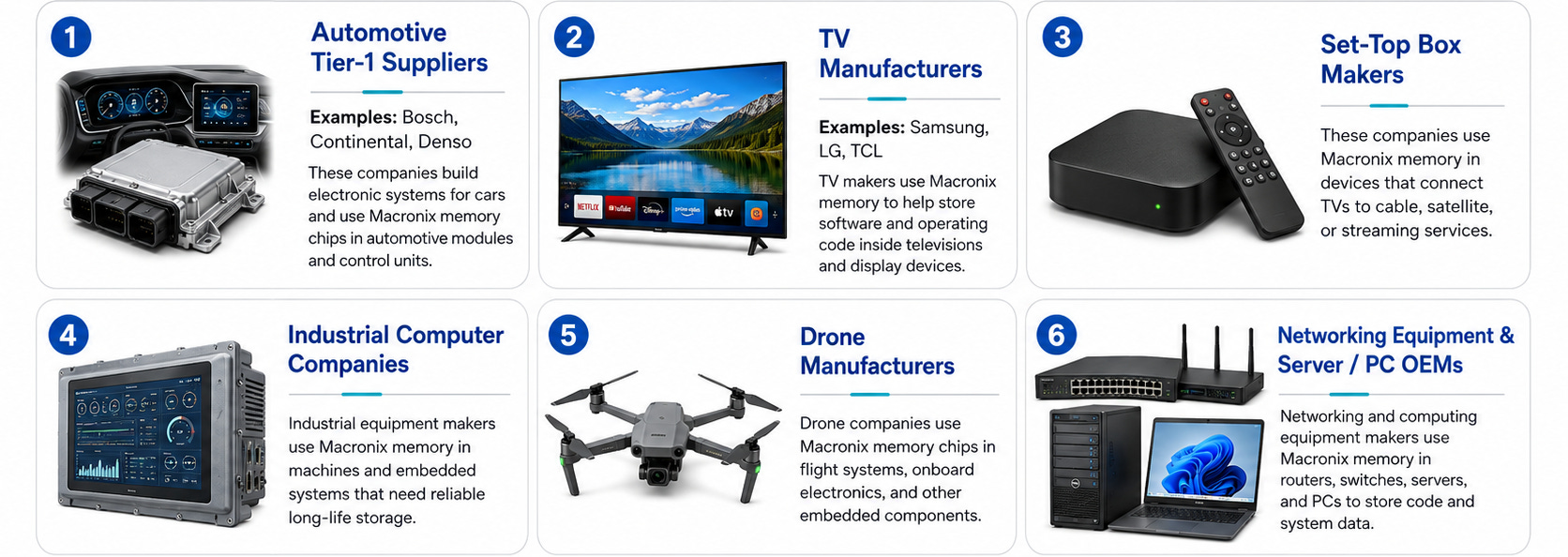

Macronix’s customers are electronics companies that build the devices in which these memory chips are used: automotive Tier-1 suppliers (Bosch, Continental, Denso), TV manufacturers (Samsung, LG, TCL), set-top box makers, industrial computer companies, drone manufacturers, networking equipment makers, and server/PC OEMs.

It also operates a small foundry business (FBG) where chips are produced on silicon wafers (wafer = the circular silicon base on which many chips are manufactured before being cut into individual dies). The 12-inch fab (Fab 5) in Hsinchu Science Park has 22,000 wafer starts per month (kwpm) and primarily produces NOR Flash, SLC NAND, ROM, and MLC/TLC NAND for eMMC products where the majority of growth comes from.

The 8-inch fab (Fab 2) has 45kwpm capacity and produces NOR Flash and foundry (FBG) products which serves as the stable base business. Macronix is increasingly pivoting into 3D TLC NAND-based eMMC at the same time that major NAND suppliers are leaving low-capacity eMMC and MLC production. Macronix has been developing 48-layer and 96-layer 3D TLC NAND capability and is ramping MLC/TLC wafer starts from roughly 1k wafers per month in 2025 to 8k by 4Q26 and 17k by 3Q27.

by investing in ASML Immersion DUV equipment to support the second phase of capacity expansion. DUV, or deep ultraviolet lithography, is equipment used to print small circuit patterns onto wafers. These tools have an estimated 18-month lead time, which makes equipment delivery timing a key constraint for the 2027 ramp.

Business Quality

On the supply side, Macronix’s key capital equipment supplier is ASML, which makes the lithography machines used to pattern circuits on silicon wafers. ASML has approximately 18-month lead times, which creates a planning constraint but not a pricing issue. Macronix is an existing customer with established relationships. The company’s ongoing raw material inputs (silicon wafers, photoresist chemicals, specialty gases) are commodity products available from multiple suppliers. No single supplier has leverage over Macronix.

On the demand side, buyers have LOW and declining negotiating power. As competitor after competitor exits MLC and SLC NAND production, Macronix’s customers have fewer and fewer alternative sources. By 2028, there will be zero alternative suppliers for low-capacity eMMC. Automotive Tier-1 suppliers (who need guaranteed 8+ year supply continuity for production vehicles) are particularly constrained as they cannot switch suppliers mid-vehicle-program without extensive requalification. In the current environment, buyers are accepting 100%+ price increases because the alternative is having no supply at all. Buyer power is structurally weak and getting weaker.

In terms of competitive landscape, building a new NAND Flash fab costs US$5-10 billion and takes 3-5 years from ground-breaking to production. No company would invest this amount to enter the MLC NAND market that every existing player is intentionally exiting because it is less profitable than TLC/QLC. The Chinese memory companies (YMTC, CXMT) are focused entirely on catching up in mainstream high-layer-count TLC/QLC NAND and DRAM for AI/data center applications. MLC is a technology the entire industry considers obsolete. In eMMC specifically, Samsung’s MLC EOL is confirmed. Micron is selling down remaining inventory and exiting. Kioxia’s tentative LTS is end of 2027. SK Hynix is actively exiting. By 2028, Macronix will be the only eMMC supplier using MLC/TLC architecture for low-capacity products. In SLC NAND, the market is consolidating to just Macronix and Winbond as Kioxia and Micron exit.

Any Threat of Substitutes? I think LOW in near/medium term, MODERATE long term. The substitute for MLC-based eMMC is TLC-based eMMC or UFS (Universal Flash Storage). Switching requires redesigning the eMMC controller IC and firmware , re-qualifying the entire module which takes 12-18 months, and paying higher component costs. Some consumer electronics demand (TVs, set-top boxes) may migrate to TLC-based alternatives over 3-5 years. But automotive, drone, industrial computer, and networking demand is sticky. However, need to closely monitor overall demand decline rate relative to a steeper supply collapse.

Revenue visibility (High). The supply-demand imbalance is locked in for 3+ years. Samsung’s MLC EOL is confirmed. Micron and Kioxia are confirmed exiting both MLC and SLC NAND. Automotive customers commit to 8-year supply agreements. The demand side declines only 13-16% annually while supply collapses 30-51%. This is not a forecast dependent on winning new customers or launching new products — it is a mathematical consequence of supply contraction.

Pricing power (High). 1Q26 confirmed pricing power across all three key product lines simultaneously. NOR Flash contract prices rose ~25% QoQ, SLC NAND +15% QoQ, and eMMC prices rose over 100% MoM in April 2026. When a company is one of few remaining suppliers in a market where customers cannot easily switch to alternatives, pricing power is structural.

Capital intensity (Medium). This is a fab business. The 12-inch fab requires ongoing equipment investment. Capex was NT$1.8B in 2025 (maintenance level), rising to NT$22.2B in 2026E and NT$20.5B in 2027E for the Phase 2 expansion (adding 10kwpm of 12-inch capacity). However, the capex is highly accretive given that every additional wafer-start generates enormous incremental revenue and margin.

Thesis 1: MLC Supply Collapse Is Irreversible

In a normal memory cycle, suppliers reduce output when profitability is weak and later add capacity when prices recover. The MLC NAND situation is different as the major suppliers are not simply cutting production temporarily but are exiting the category.

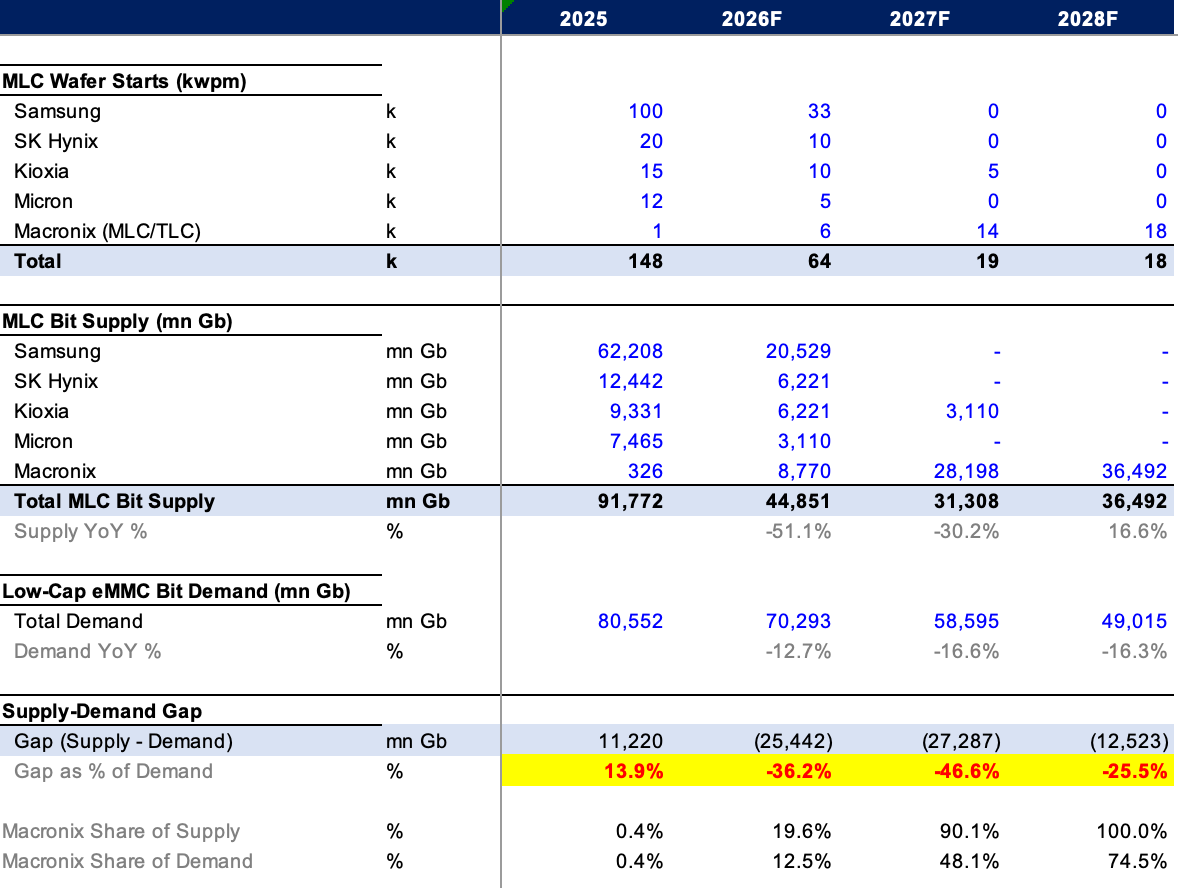

Samsung announced MLC end-of-life in October 2025, which means that they are formally ending production or support for a product. Commercial customer last-time-ship ( the final date when customers can receive shipments) was end of 1Q26, while automotive LTS is end of 3Q26. Samsung’s MLC wafer starts decline from 100k in 2025 to 33k in 2026E and then to zero from 2027 onward. More importantly, Samsung is removing MLC-capable equipment from its fabs. Once equipment is removed and fab space is converted to other products, the capacity becomes much harder to restore.

SK Hynix is also exiting MLC. Wafer starts decline from 20k in 2025 to 10k in 2026E and then to zero in 2027E. The company is reallocating cleanroom space (i.e. controlled manufacturing area inside a fab where chips are produced) to HBM and advanced DRAM given that they command much higher margins than legacy MLC NAND, so large memory suppliers have a strong incentive to shift scarce manufacturing capacity toward those products.

Kioxia has set a tentative LTS of end-2027. Its wafer starts decline from 15k in 2025 to 10k in 2026E, 5k in 2027E, and then zero in 2028E.

Micron has notified automotive customers and module houses of its MLC exit. A module house buys memory chips and assembles them into finished storage products or modules. Micron’s remaining supply is largely inventory drawdown, meaning it is selling existing stock rather than maintaining long-term production. Its wafer starts decline from 12k in 2025 to 5k in 2026E and then to zero in 2027F.

Total global MLC wafer starts collapse from 148k in 2025 to 64k in 2026E, 19k in 2027F, and 18k in 2028F. By 2028, Macronix is expected to be the only remaining supplier. Global MLC bit supply declines from 91.8B Gb in 2025 to 44.9B Gb in 2026E and 31.3B Gb in 2027E, representing declines of 51% and 30%, respectively.

Thesis 2: Switching Costs and TLC Shortage Prevent Demand Substitution

The main bear case is that low-capacity eMMC demand can migrate to TLC-based alternatives. This is possible in theory, but constrained in practice.

First, there are performance and design differences. Multiple small-capacity MLC dies can sometimes deliver better IO speeds than a single equivalent-capacity TLC die. IO, or input/output, refers to how efficiently data can be read from or written to memory. This matters in automotive, drone, industrial PC, and networking applications where reliability, latency, and consistency are important.

Second, eMMC is not just a memory chip. It includes NAND, a controller, and firmware. The controller manages how data is written, stored, corrected, and read. Firmware is the low-level software inside the device that controls how the hardware operates. Switching from MLC to TLC NAND often requires firmware rewrites and, in some cases, full controller redesigns. This can involve expensive mask sets and long qualification cycles. For commercial applications, qualification can take 12-18 months. For automotive-grade parts, the process can take even longer because customers need to validate reliability, durability, and long-term supply availability.

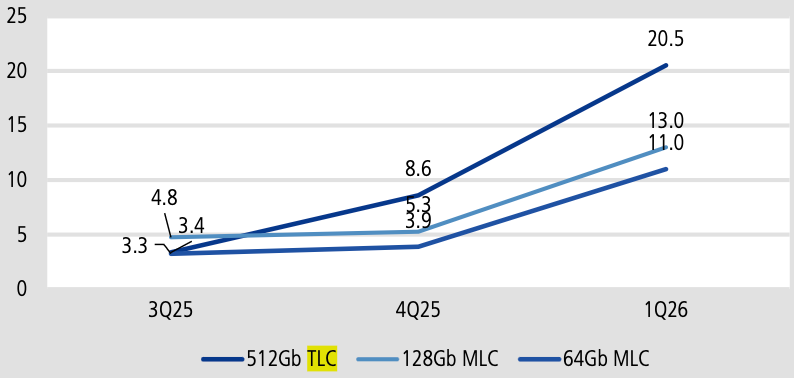

Third, current pricing also weakens the substitution argument. 512Gb TLC die prices are around US$20.50 in 1Q26, compared with roughly US$13 for 128Gb MLC and US$11 for 64Gb MLC. This means TLC is not obviously cheaper, especially after factoring in redesign, validation, and qualification costs.

MLC v. TLC Pricing

Thesis 3: Macronix’s Capacity Ramp Creates an Earnings Explosion

Macronix is aggressively reallocating its 12-inch fab toward MLC/TLC NAND production. The ramp trajectory is as follows:

2025: roughly 1k wafers per month of MLC/TLC NAND, mostly using the 2D 19nm process for 2GB / 4GB / 8GB eMMC

1Q26E: 2k wafers per month

2Q26E: 7k wafers per month, driven by ROM and R&D reallocation plus roughly 3k of new capacity

3Q26E-4Q26E: 7k-8k wafers per month

1Q27E-2Q27E: 10k wafers per month as second-phase equipment arrives

3Q27E-4Q27E: 17k wafers per month after ASML DUV tools are fully installed

The ramp matters because it combines two forms of output growth. First, Macronix is allocating more wafers to MLC/TLC NAND. Second, the transition to 3D TLC NAND increases the amount of storage capacity produced per wafer.

Total eMMC bit output grows from 326M Gb in 2025 to 8,770M Gb in 2026E and 28,198M Gb in 2027F. That represents 2,590% YoY growth in 2026 and 222% growth in 2027. At the same time, eMMC ASP/Gb rises from US$0.07 in 2025A to roughly US$0.29 in 2026E and US$0.36 in 2027E. The ASP assumptions are lower than prior estimates because higher-capacity eMMC products carry lower ASP/Gb, but they still imply a major pricing uplift versus 2025.

In short, Macronix is expected to ship many more bits while also earning more revenue per bit.

Valuation

At the current price of NT$160, the stock trades at about 5.3x 2026E EPS or 1.5x 2027E EPS. The closest historical comp is Nanya Technology during the DDR4 shortage cycle. As the primary listed beneficiary of tightening DDR4 supply, Nanya re-rated to roughly 8–12x FY1E EPS as investors began underwriting peak-cycle earnings power. Macronix presents a similar setup today, with eMMC moving from a small revenue contributor to the dominant driver of earnings. Given the severity of the MLC/eMMC supply gap and the magnitude of the EPS inflection, a 10x FY26E EPS multiple does not appear aggressive. That framework implies a NT$300 price target, with upside risk if estimates continue to revise higher and the market starts viewing Macronix as the core listed beneficiary of the eMMC shortage cycle.

However, the Macronix setup appears structurally superior:

the supply exit is permanent rather than cyclical

Macronix may become a monopoly supplier, while Nanya remained one of several DDR4 producers.

The demand tail is longer because automotive and industrial customers face long qualification cycles and are less likely to switch suppliers quickly.

Where Could Our Thesis Go Wrong

1. Equipment Delivery Delays

The second phase of capacity expansion depends on ASML Immersion DUV tool delivery, currently at roughly 18-month lead times. Any delay could push the 3Q27 ramp target into 4Q27 or later, reducing 2027 bit output and revenue estimates. This presents the largest execution risk because current estimates depends heavily on Macronix reaching the planned 17k wafers per month capacity target.

2. Faster-Than-Expected Demand Substitution to TLC — Medium-High

If TLC NAND supply loosens faster than expected, customers may migrate away from MLC-based eMMC more quickly. This could happen if Samsung expands NAND output more aggressively at P4 or if YMTC ramps faster than expected.

Faster migration would narrow the pricing premium for MLC-based eMMC and reduce Macronix’s pricing power. I view this as unlikely given industry prioritization of DRAM and HBM, but it remains the most important demand-side risk.

3. Customer Qualification Timelines — Medium

Macronix’s 3D TLC NAND eMMC products, including 8GB, 16GB, and 32GB versions, are expected to begin wafer-in during 2Q-3Q26.

If automotive or industrial qualification takes longer than expected, volume shipments could be delayed by one to two quarters. This would push back the earnings ramp even if the long-term thesis remains intact.

4. Yield Risk

The 3D NAND ramp depends on Macronix achieving acceptable yields on 48-layer and 96-layer TLC NAND. Yield refers to the percentage of chips that work properly after production.

Key Drivers

2Q26: First 3D TLC NAND eMMC products (8GB/16GB commercial and industrial grade) begin wafer-in. eMMC contract prices raise QoQ.

3Q26: 32GB commercial-grade eMMC wafer-in. Continued pricing momentum

4Q26: MLC/TLC wafer starts reach 8k wpm.

1Q-2Q27: Second phase equipment installation begins. Investors begin pricing 2027E earnings power.

3Q27: MLC/TLC wafer starts reach 17k wpm. Bit output enters exponential growth phase. By this point, Macronix is the only remaining low-capacity eMMC supplier globally.

2028+: Samsung, SK Hynix, Kioxia, and Micron have fully exited MLC. Macronix holds monopoly position in a market with persistent demand from automotive, drone, IPC, and networking applications. Long-term earnings sustainability thesis is either validated or challenged.